Amazing Emergency Fund Calculation India: Your Crucial Guide to Financial Safety

We’re going to talk about something super important today: your emergency fund calculation India! Ever had one of those “oops” moments where something unexpected pops up, and suddenly your wallet feels a bit light? Maybe your phone decided to take a swim, or your scooter needed a surprise repair. Life’s full of surprises, right And that’s exactly why we’re going to talk about emergency fund amount india

Think of an emergency fund as your financial superhero cape. It swoops in to save the day when unexpected bills try to ruin your budget. No more stressing when life throws a curveball! This article is your friendly guide to building a strong financial safety net in India, so let’s dive in!

Why Even Bother with an Emergency Fund? Because Life Happens!

You might be thinking, “Do I really need a separate fund just for emergencies?” And the answer is a resounding YES! Imagine your financial life as a smooth-sailing ship. An emergency fund is like having extra life rafts and a backup engine. When a storm (read: unexpected expense) hits, you won’t sink!

Lately, financial experts have noted that Indian households, while traditionally good savers, are increasingly taking on debt just to cover everyday needs, not to build assets. This trend is backed by recent data that highlights the silent surge in household debt, as reported by outlets covering the Reserve Bank of India (RBI) findings (Deccan Herald – The silent surge in India’s household debt). Without a dedicated emergency corpus India, you could be forced into this risky cycle of borrowing just to pay the bills!

Here are a few common “storms” an emergency fund helps you weather:

- Job Loss: Losing your job can be stressful enough without worrying about how you’ll pay rent or buy groceries.

- Medical Emergencies: Unexpected health issues can strike anyone, and hospital bills can be substantial.

- Home Repairs: A leaky roof or a broken geyser usually pops up at the worst time.

- Car/Bike Trouble: Unexpected vehicle repairs can put a big dent in your monthly budget.

Without an emergency fund, you might end up doing things you regret, like taking out expensive loans or racking up credit card debt. And trust me, nobody wants that!

The Hidden Costs of NOT Having an Emergency Fund

When you don’t have an emergency corpus India, those unexpected expenses often don’t just go away. Instead, they force you into less-than-ideal financial choices. This chart shows how people often cope when they lack an emergency fund:

The chart clearly shows the financial pain points – from high-interest debt to draining your future investment plans. This is exactly what your accurate emergency fund calculation India helps you avoid!

The Golden Rule: Your 3 to 6 Months Expenses India Target

This is where the true “emergency fund calculation India” comes into play! A general rule of thumb that experts worldwide, including those in India, recommend is to have 3 to 6 months of your essential living expenses saved up.

“Whoa, 3 to 6 months? That sounds like a lot!” you might be thinking. And yes, it can seem daunting at first, but breaking it down makes it much more manageable.

Let’s Break Down the Calculation:

- List Your Essential Monthly Expenses: Grab a pen and paper (or open a spreadsheet!). What are the absolute must-pay bills every single month?

- Rent/Home Loan EMI

- Groceries

- Utilities (electricity, water, gas)

- Basic transportation/loan EMIs

- Insurance premiums (Health and Term Life)

- Basic school fees

Self-care expenses, dining out, subscriptions, or entertainment are NOT essential in a true emergency. These are “wants,” not “needs.” If you want to learn how to track and manage your entire budget, make sure you start by tracking these exact essential numbers!

- Calculate Your Total Essential Monthly Expenses: Add up all those numbers. Let’s say, for example, your essential monthly expenses come out to ₹45,000.

- Multiply by 3 to 6 Months:

- For a 3-month fund: ₹45,000 x 3 = ₹1,35,000

- For a 6-month fund: ₹45,000 x 6 = ₹2,70,000

So, in this example, your ideal emergency fund amount in Rupees would be between ₹1,35,000 and ₹2,70,000.

Which Amount is Right for You?

The choice between a 3-month and a 6-month fund often depends on your job and family situation:

| Situation | Recommended Months | Why? |

| Stable Job (Govt/Large Company) | 3 Months | You’re less likely to lose your job, and if you do, finding another might be quicker. |

| Multiple Income Earners | 3-4 Months | If one person loses a job, the other’s income can help buffer the shock. |

| Self-Employed/Uncertain Income | 6-12 Months | Your income stream is variable, requiring a larger safety net for lean months. |

| Sole Earner with Dependents | 6 Months + | You have more people relying on you, so the financial impact of a job loss is greater. |

The goal is to aim for at least 3 months and then gradually build it up to 6 months or more if your circumstances suggest it. This gives you a really strong emergency corpus India to rely on.

Where Should I Keep My Emergency Fund? Liquidity is Your Superpower!

You know your target. Now, where do you put this precious money? This is super important! Your money needs to be Safe and Easily Accessible (Liquid).

Here are the best options for your ideal emergency fund amount in Rupees in India:

- Savings Bank Account: Safe and instantly liquid. The interest rates are typically low (around 2.5% to 4%), which means your money doesn’t grow much. Use this for the small portion you might need immediately.

- Fixed Deposits (FDs) with a Sweepin/Flexi Facility: These FDs automatically break when your linked savings account balance runs low. They offer slightly better interest than a regular savings account.

- Liquid Mutual Funds for Emergency Fund: This is often the smartest choice for the bulk of your fund!

- Why they are great: They usually offer higher returns than a savings account and are highly liquid. You can often redeem your money within 24 hours (T+1), and many fund houses even offer instant redemption up to ₹50,000 or more via UPI!

- For a detailed look at whether liquid mutual funds for emergency fund are right for you, and to understand their tax benefits, it’s worth checking out resources from the Association of Mutual Funds in India (AMFI) for authentic information (AMFI India – Mutual Fund Basics).

Remember: Avoid keeping this money in risky investments like stocks or regular equity mutual funds, as the value can drop right when you need it!

Let’s Visualize the Difference in Returns!

This chart shows how different storage options perform on a hypothetical amount of money. Since this is your safety net, you want it to at least keep up with inflation!

(Please note: These are illustrative returns and actual returns can vary based on market conditions and specific fund performance. Always check current rates and fund details.)

As you can see, while all options keep your money safe and accessible, some work a little harder for you!

Building Your Emergency Fund: Small Steps Lead to Big Savings!

Now that you know the “what” and “where,” let’s talk about the “how”! Building your emergency corpus India doesn’t have to be overwhelming.

- Set a Clear Goal: Based on your emergency fund calculation India, determine your target amount (e.g., ₹1,80,000).

- Make it Automatic: Set up an automatic transfer from your salary account to your emergency fund account (or investment in a liquid fund) every month. Even ₹1,000 or ₹2,000 consistently adds up!

- Cut Down and Redirect: Take a hard look at your non-essential spending. Can you cut one expensive restaurant meal a month? That money goes straight to your fund! If you need help, our site has guides on easy ways to save money every month.

- Use Windfalls Wisely: Did you get a bonus, a tax refund, or a cash gift? Consider putting a good portion of it straight into your emergency fund.

- Track Your Progress: Seeing your emergency fund grow can be incredibly motivating! Use an app, a spreadsheet, or even a simple notebook to track your progress towards your ideal emergency fund amount in Rupees.

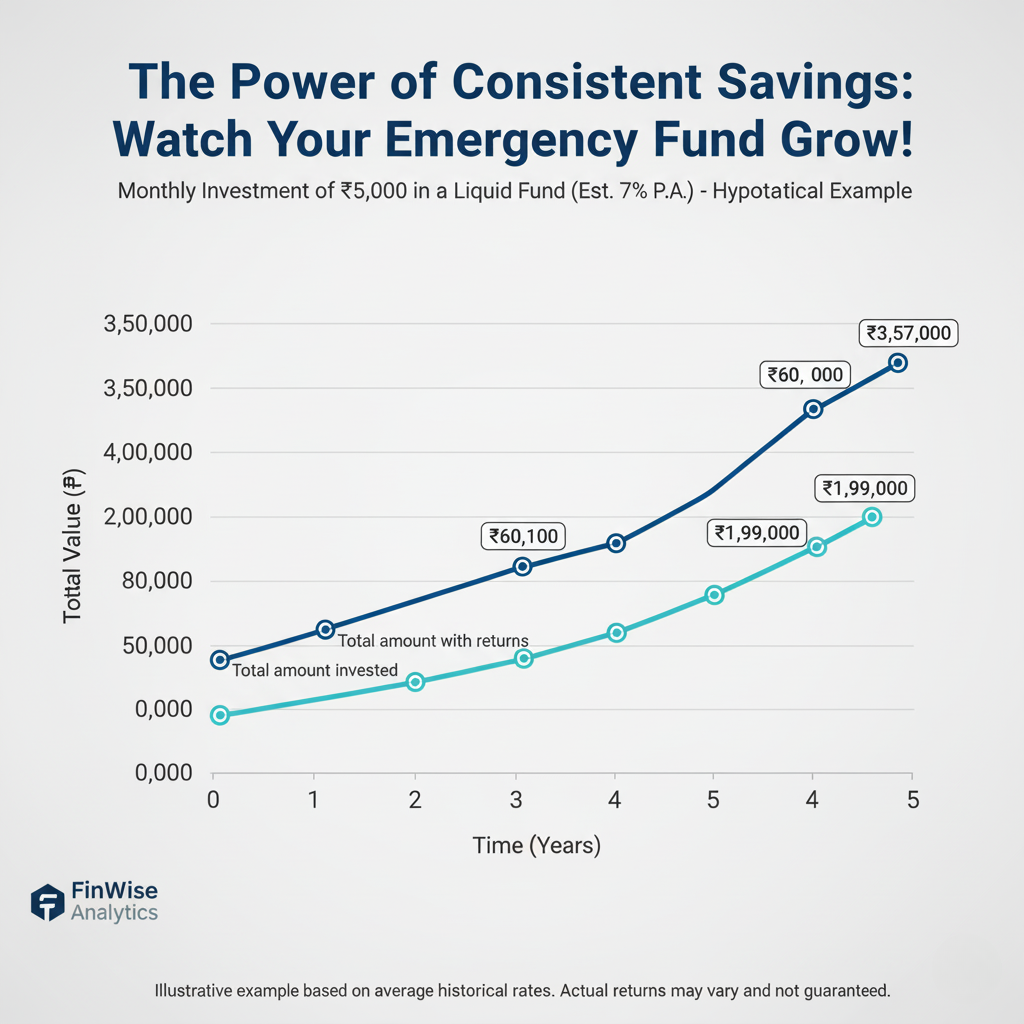

Watch Your Emergency Fund Grow Over Time!

Even small, consistent savings can lead to a significant emergency corpus India. Let’s look at an example. If you decide to save ₹5,000 every month and keep it in a liquid mutual fund earning an average of 7% per year, here’s how your fund could grow:

| Year | Total Saved (Your Contribution) | Total Corpus Value (Approx. 7% Return) |

| 1 | ₹60,000 | ₹62,000 |

| 2 | ₹1,20,000 | ₹1,28,000 |

| 3 | ₹1,80,000 | ₹1,95,000 |

| 4 | ₹2,40,000 | ₹2,69,000 |

In just four years, you’ve built a massive safety net that can cover nearly 6 months of the ₹45,000 monthly expense we used in our example! This proves that small steps lead to an amazing financial result.

Maintaining Your Emergency Fund: Don’t Dip Into It for Non-Emergencies!

This is crucial! Your emergency fund is only for true emergencies. It’s not for:

- That new gadget you’ve been eyeing.

- A fancy vacation.

- A sale on your favorite clothes.

- Investing in the stock market (unless it’s a separate investment fund).

If you use it for something that’s not a genuine emergency, you’ll have to start building it all over again, and that can be discouraging. Think of it as a “break glass in case of emergency” situation – you only use it when absolutely necessary!

When You Do Use It, Replenish It!

If an actual emergency does occur and you have to dip into your fund, that’s okay! That’s what it’s there for. But as soon as the emergency passes, make it your priority to replenish the fund back to your target emergency corpus India amount. Treat it like a loan you’ve taken from yourself that needs to be paid back promptly.

Beyond the Emergency Fund: What’s Next?

Once you have your solid 3 to 6 months expenses India covered in your emergency fund, you’re in an amazing financial position! What’s next?

- Debt Repayment: Tackle any high-interest debts like credit card bills.

- Investments: Start investing for your long-term goals like buying a house, your child’s education, or retirement.

- Insurance: Ensure you have adequate health and life insurance to protect your family from major financial shocks.

Remember, building wealth and financial security is a journey, not a sprint. Start with your emergency fund, and you’ll be well on your way to a brighter financial future!

Frequently Asked Questions (FAQs)

What is the 3-6-9 Rule in Finance?

The “3-6-9 rule” often refers to a guideline for emergency fund savings in personal finance, especially in the context of job stability and income:

- 3 Months of expenses for people with high job stability (like government jobs or essential services).

- 6 Months of expenses for people with average stability (most salaried professionals).

- 9 Months (or more) of expenses for people with highly variable income, like freelancers, entrepreneurs, or those in volatile industries. It dictates the minimum safety net you should maintain.

What is the 7-5-3-1 Rule in SIP?

The 7-5-3-1 rule is a popular thumb rule used to help investors estimate the impact of inflation on their SIP (Systematic Investment Plan) goals in India. It suggests that a SIP goal corpus targeted for a certain number of years from now should be multiplied by the following factors to account for long-term inflation:

- 7x for a goal 20 years away.

- 5x for a goal 15 years away.

- 3x for a goal 10 years away.

- 1x for a goal 5 years away. The numbers are intended to simplify inflation’s effect, meaning you need to save significantly more than the current cost of your goal.

Is 1 Crore Enough to Survive in India?

₹1 crore is generally not enough for a long retirement in India, although it can provide a decent cushion for a few years. Whether it’s “enough to survive” depends entirely on your lifestyle, city of residence (cost of living is much higher in Mumbai or Bengaluru than in a Tier-2 city), age, and expected lifespan. Assuming a withdrawal rate of around ₹4-5 lakh per year and increasing inflation, this amount could be depleted in about 20-25 years. It serves as a good base but not a full retirement corpus.

What is the 50/30/20 Rule of Money in India?

The 50/30/20 rule is a simple budgeting guideline popular in India and globally, recommending how you should split your post-tax income:

- 50% for Needs (essentials like rent, groceries, utility bills, loan EMIs).

- 30% for Wants (discretionary spending like dining out, entertainment, shopping, subscriptions).

- 20% for Savings and Debt Repayment (contributions to an emergency fund, investments like SIPs, and clearing high-interest debt like credit cards).

What is the 70/20/10 Rule Money?

The 70/20/10 rule is another variation of a budgeting principle, typically suggesting the following allocation of post-tax income:

- 70% for Spending (covering both essential needs and discretionary wants).

- 20% for Savings and Investments (building wealth, retirement funds).

- 10% for Debt Repayment or Charity (focusing on accelerating debt payoff or giving back). It’s a less granular approach than the 50/30/20 rule.

How long will $500,000 last using the 4% Rule?

The 4% Rule suggests that you can safely withdraw 4% of your total retirement corpus in the first year of retirement, and then adjust that amount for inflation annually, with a high probability (historically over 90%) of the money lasting for 30 years. Using this rule:

- An initial withdrawal of 4% of $500,000 is $20,000.

- Therefore, $500,000 is theoretically expected to last for 30 years, provided you maintain a diversified portfolio and annual withdrawals are adjusted for inflation.

What is Warren Buffett’s 90/10 Rule?

Warren Buffett’s 90/10 rule is a simple investment strategy he famously recommended for the money left to his wife:

- 90% of the money should be put into a low-cost S&P 500 index fund (a highly diversified, low-risk investment tracking the U.S. stock market).

- 10% should be invested in short-term government bonds (for stability and safety). The rule advocates for a low-fee, long-term, passive investing approach over trying to pick individual stocks.

How to turn $10,000 into $100,000 quickly?

There is no guaranteed, safe, or legal method to turn $10,000 into $100,000 quickly. This is a 10x return, which typically requires taking extremely high risk through ventures like highly speculative trading (e.g., penny stocks, high-leverage crypto), starting a high-risk/high-reward business, or gambling. For nearly all investors, attempting this is likely to result in the loss of the initial $10,000 rather than achieving the target.

Which SIP gives 40% return?

No SIP (Systematic Investment Plan) or mutual fund guarantees a 40% return. A 40% return is considered exceptionally high, usually only achieved during temporary bull market peaks or by highly aggressive sector-specific funds over short, specific periods. A realistic long-term return expectation for a diversified equity SIP in India is typically between 12% and 15% per annum. Beware of any product promising guaranteed returns this high, as it carries very high risk.

Can I retire at 55 with 1 million?

Whether you can retire at age 55 with $1 million (approx. ₹8.3 crore) depends heavily on your lifestyle and location. In a high-cost country or city, it might be challenging. In India, using the 4% withdrawal rule (or ₹33.2 lakh annually), it offers a good chance of lasting 30 years or more, especially if combined with social security or rental income. For a comfortable retirement starting at 55, this is a strong starting point, but careful budgeting and conservative withdrawal are essential.

What is a top 1% salary in India?

Defining a “top 1% salary in India” is complex as figures vary greatly by year, data source, and city (Mumbai vs. a smaller town). Generally, to be considered in the top 1% of earners in India, an individual needs to earn an Annual Income of ₹30 lakh or more. For the absolute top tier, especially in metro cities, this figure can often exceed ₹1 crore annually.

Can I retire at 40 with 2 crore in India?

Retiring at age 40 with ₹2 crore is extremely challenging and risky. Given that you would need the corpus to last for 40-50 years (until age 80-90), the rate of withdrawal must be very low to sustain the fund against inflation. A safe withdrawal of 4% (₹8 lakh per year) is barely enough for a modest lifestyle in a Tier-2 city today. To retire that early, most financial planners recommend a corpus of at least ₹5-10 crore, depending on your lifestyle.

How much should I have saved for retirement by age 45 in India?

A common rule of thumb for retirement savings suggests having a corpus equal to 3 to 4 times your current annual salary saved by age 45. However, a more accurate goal is based on retirement planning (which requires 25-30 times your annual expenses).

- A simpler goal for India is to have about 40% of your total target retirement corpus saved and invested by age 45 to be on track, given the accelerated growth required in the later years.

How long will 5000000 last in retirement?

₹50,00,000 (₹50 lakh) will not last very long in retirement.

- If you withdraw a conservative ₹30,000 per month (₹3.6 lakh/year), the money would be depleted in roughly 15 years without considering inflation or any growth.

- When accounting for 6-7% inflation, the purchasing power will drop rapidly, and the corpus will likely last less than 15 years unless you live in a very low-cost area or have other guaranteed income sources.

How much cash can I keep at home legally in India in 2025?

There is no specific limit on the amount of cash you can keep at home legally in India. However, the income tax department places restrictions on certain cash transactions to curb black money:

- You cannot accept or repay a loan/deposit over ₹20,000 in cash.

- You cannot receive cash of ₹2 lakh or more in total from a single transaction with a single person in a day.

- If the cash you hold is sourced from legitimate, taxed income and you can prove the source with proper documentation, any amount is generally permissible. If a search occurs, you must be able to justify the source of the funds.