The #1 ULTIMATE Dave Ramsey Saving Chart: Fix Your Finances NOW

Dave Ramsey saving chart. If you’re here, that’s what you need. You’re tired of the panic. You’re tired of the worry.

Ever had your car break down the same week the washing machine died? That feeling of instant panic, where you know your wallet is about to take a massive hit?

If that happens and you don’t have a plan, most people grab the nearest credit card. That’s how the debt cycle starts.

This is not a small problem. It’s the reason most people feel stuck.

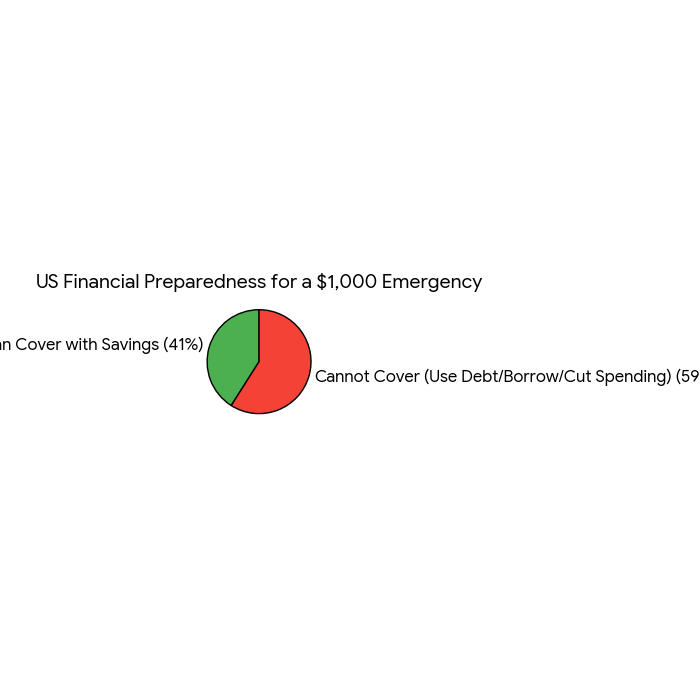

The raw data shows the financial exposure of most US households. A 2025 Bankrate survey found that 59% of Americans cannot afford an unexpected $1,000 emergency expense using their savings alone (Source).

To see this financial reality clearly, look at the prepared versus the unprepared:

Visualizing the $1,000 Emergency Gap

This chart shows that only 41% of people are prepared to cover a small emergency with cash, leaving the majority financially exposed. This visual explains why that emergency fund amount dave ramsey suggests is so powerful: it instantly moves you into the minority of prepared Americans.

If you’ve heard of the money guy, Dave Ramsey, you know he’s all about creating this shield before you do anything else. He uses simple steps, often called the Baby Steps, and the first few are all about creating your emergency safety net.

Let’s break down the official dave ramsey saving chart and show you exactly how to build yours, starting right now.

Step 1: The Starter Emergency Fund ($1,000)

You’re probably wondering, How much does Dave Ramsey recommend for an emergency fund?

The very first goal is small, but it’s the most important for your mindset.

Dave Ramsey calls this Baby Step 1: Save $1,000 for your Starter Emergency Fund.

Why only $1,000?

- It’s a Fire Extinguisher: This $1,000 is for the small stuff. It’s for a flat tire, a quick trip to the ER, or a minor repair. It stops small emergencies from turning into brand new debt.

- It’s a Quick Win: It gives you a burst of confidence. If you can save $1,000 quickly, you know you can save more later.

- It’s a Requirement: You MUST finish this step before paying off debt (Baby Step 2). If a surprise bill hits while you’re paying off debt, you’ll just go back into debt, totally wrecking your progress.

Remember, nearly two-thirds of Americans don’t have this simple buffer. The consequences of not having it are clear when you look at what people rely on.

Where Does the Money Come From When Savings Run Out?

When savings aren’t enough, people use various forms of debt and borrowing. Look at the breakdown of how Americans would cover that same $1,000 emergency:

Notice how Credit Card (25%) is the top choice after savings. Your $1,000 fund literally prevents you from falling into that trap, avoiding high interest rates and the Debt Snowball.

Chart 3: Your $1,000 Starter Fund Tracker

For a new saver, getting to $1,000 can feel like climbing a mountain. This tracker helps you turn the number into a concrete goal:

| Goal | Amount to Save | Status | ||

| 25% Complete | $250 |

$$ $$

|

||

| 50% Complete | $500 |

$$ $$

|

||

| 75% Complete | $750 |

$$ $$

|

||

| 100% Complete | $1,000 | $$ X \/ $$ |

Pro Tip: If you can’t hit that goal fast, break it down smaller! Think of ways to find extra cash: Sell something on Facebook Marketplace, pick up a short-term side hustle, or cut out all eating out. Every $50 contributes to your emergency fund amount dave ramsey goal.

Step 2: Pay Off All Debt (Except the House)

Once you have your little $1,000 fire extinguisher, it’s time to go to war on your debt.

Dave Ramsey is famous for the Debt Snowball Method. This is the key to Baby Step 2.

The goal here is simple: Pay off all debt except for your home mortgage.

How the Debt Snowball Works

The Debt Snowball is all about psychology and momentum, not math.

- List all your non-mortgage debts from the smallest balance to the largest balance. Ignore the interest rate.

- Attack the smallest debt with the biggest payments you can manage. Only pay the minimum on everything else.

- When the smallest debt is gone, take the entire payment you were making on it and roll it into the next smallest debt.

This creates a psychological “snowball” that grows faster and faster, keeping you motivated as you get quick wins.

For example: Say you have a $500 credit card bill and a $5,000 student loan. You pay off the $500 card first. The relief and excitement you feel will keep you going, even though the student loan has a higher interest rate.

Step 3: The Full Emergency Fund (3-6 Months of Expenses)

Once Baby Step 2 is complete—you are debt-free except for the house—you move on to building the real financial fortress.

Now you need to ask yourself, How much money should I have in savings for emergency fund?

Dave Ramsey recommends 3 to 6 months of essential living expenses. This is your serious financial shield. It’s there for big emergencies like:

- Job loss

- Major medical bill

- Long-term disability

Calculating Your Full Goal

You have to figure out your true monthly expenses first. You don’t save for fun money, just your necessities.

Necessity Expenses Only:

- Housing (Rent/Mortgage)

- Utilities (Electric, Water, Gas)

- Food (Groceries, not dining out)

- Transportation (Gas, basic insurance)

- Basic Insurance (Health, Life, Car)

Example: Finding Your Final Goal

If your total essential expenses come out to $3,500 per month, your goal looks like this:

| Months to Save | Calculation | Total Emergency Fund Goal |

| 3 Months | $3,500 $\times$ 3 | $10,500 |

| 6 Months | $3,500 $\times$ 6 | $21,000 |

This completed amount becomes your official dave ramsey saving money chart goal.

Should You Save 3 Months or 6 Months?

This decision makes your plan personal. It’s about your risk level.

- Aim for 3 Months if:

-

- You are single and have a very stable job (low risk of layoff).

- You are married and both partners have stable, similar-level incomes.

- Aim for 6 Months if:

-

- You or your spouse is self-employed (income is irregular).

- You work solely on commission or have seasonal employment.

- You have several young children or family members relying on you.

The Secret to Getting the Cash: The 20/80 Rule

The reason Ramsey’s method works isn’t just because of the math.

He often talks about the financial principle that 80% of personal finance is behavior, and 20% is head knowledge (math). This is the 20 80 rule Dave Ramsey refers to.

It means that no budget spreadsheet will save you if you can’t control your spending habits. The Baby Steps force you to change your behavior by giving you small wins (Baby Step 1) followed by massive motivation (Baby Step 2: Debt Snowball).

For example, my friend Sarah finished her $1,000 fund just a month before her dog needed emergency surgery. Instead of adding a $600 vet bill to her credit card, she calmly transferred the money from her dedicated savings account. No panic. No debt. That is the power of the plan.

Answering Your Burning Questions (FAQ)

How much does Dave Ramsey say you should save?

It depends on the step: $1,000 to start (Baby Step 1), and then 3 to 6 months of essential living expenses for the full fund (Baby Step 3). After that, he recommends investing 15% of your household income into retirement (Baby Step 4).

Is $25,000 a good emergency fund?

Yes, probably. Unless you have massive monthly expenses, $25,000 is likely enough to cover 3 to 6 months. Is 30k too much for an emergency fund? Only if it is far more than 6 months of expenses and is sitting in a low-interest account. The excess cash should be moved into investments (Baby Step 4).

What is the rule of 55 Dave Ramsey?

The “Rule of 55” is an IRS tax rule, not an official Dave Ramsey Baby Step. It allows workers who leave a job (or are laid off) in the year they turn 55 or older to withdraw from their current job’s 401(k) or 403(b) penalty-free (Source).

What percent of Americans live paycheck to paycheck?

In 2023, nearly two-thirds of U.S. consumers (64%) reported living paycheck to paycheck (Source). This statistic clearly shows why building an emergency fund is the first, crucial step toward financial stability.

How many Americans have 100k in savings?

It’s difficult to find an exact liquid savings number, but statistics suggest that only about one in five Americans have $100,000 or more in combined savings and investment accounts. Hitting this number is usually achieved through dedicated investing (Baby Steps 4-7), not just an emergency fund.

One Comment