Dave Ramsey Emergency Fund: Why $1,000 is Just the START

Dave Ramsey Emergency Fund. You see the term everywhere. Maybe you’re wondering: Who is this guy, why should I listen to him, and what exactly is his emergency fund plan?

You’re not alone. Dave Ramsey has created the most popular financial roadmap in America, and it all starts with saving money. If you’ve been struggling with debt and feeling stressed, you need this clarity.

Let’s break down the two critical amounts of the Dave Ramsey Emergency Fund and why following them in order is non-negotiable.

Who is Dave Ramsey and Why Does His Plan Matter?

Who is Dave Ramsey?

Dave Ramsey (David Lawrence Ramsey III) is a popular American finance personality and radio host. He is the founder of Ramsey Solutions.

- The Intentions: He created his plan after he went from a $4 million real estate empire to bankruptcy in 1988. This traumatic experience convinced him that traditional debt models are dangerous. His mission is to show people how to achieve “financial peace” by avoiding debt completely and building wealth through cash, savings, and long-term investing.

- The Philosophy: His entire system is based on the idea that personal finance is 80% behavior and only 20% knowledge. The Baby Steps are designed to change your habits first.

What is the Dave Ramsey Emergency Fund?

The Dave Ramsey Emergency Fund is a cash buffer saved in two separate stages to protect you from life’s biggest emergencies. Unlike some financial pros, Dave says your emergency fund must be saved before you start investing.

Baby Step 1: The First Financial Shield

The $1000 Starter Emergency Fund

The first required amount in the Dave Ramsey Baby Steps is not a full fortress; it’s a small fire extinguisher.

What it is exactly: You must save $1,000 cash in an easily accessible savings account.

| Why This Amount Works | Why It’s Step 1 |

| It’s Achievable: Most people can find $1,000 fast by selling items, getting a side gig, or cutting everything non-essential for a month. | It Stops the Bleeding: Before you attack debt, you need a defense. A flat tire or a vet bill will happen, and without this cash, you’ll just borrow money again, crushing your motivation. |

The Hard Truth: According to a 2025 Bankrate survey, 59% of Americans cannot afford an unexpected $1,000 emergency expense using savings alone (Source). By completing this step, you instantly move yourself into the financially secure minority.

Baby Step 2: Pay Off All Debt (The Debt Snowball)

Once you have your $1000 Starter Emergency Fund, you pause saving and dedicate every extra dollar to debt payoff.

- You pay off all non-mortgage debt (credit cards, car loans, student loans) from smallest balance to largest balance. This is the Debt Snowball.

- This intense focus frees up your income so that when an emergency hits, you are no longer making those minimum payments.

Baby Step 3: Building the Financial Fortress

The Fully Funded Emergency Fund (3-6 Months Expenses)

Once the debt is gone (Baby Step 2 is finished), it’s time to complete your protection. This is your Fully Funded Emergency Fund.

What it is exactly: 3-6 Months Expenses saved in a high-yield savings account.

Your goal isn’t just to save a random amount; it’s to save your survival budget for 3-6 Months Expenses so you can survive the worst financial crises, like job loss, without touching debt or investments.

How To Calculate Your Amount

- Calculate Survival: Tally your strict, essential monthly expenses (housing, utilities, basic food, insurance).

- Determine Risk: Multiply that survival budget by 3 and 6.

| Risk Level | Financial Goal | Example ($4,000 Survival Budget) |

| Lower Risk | 3 Months Expenses | $12,000 |

| Higher Risk | 6 Months Expenses | $24,000 |

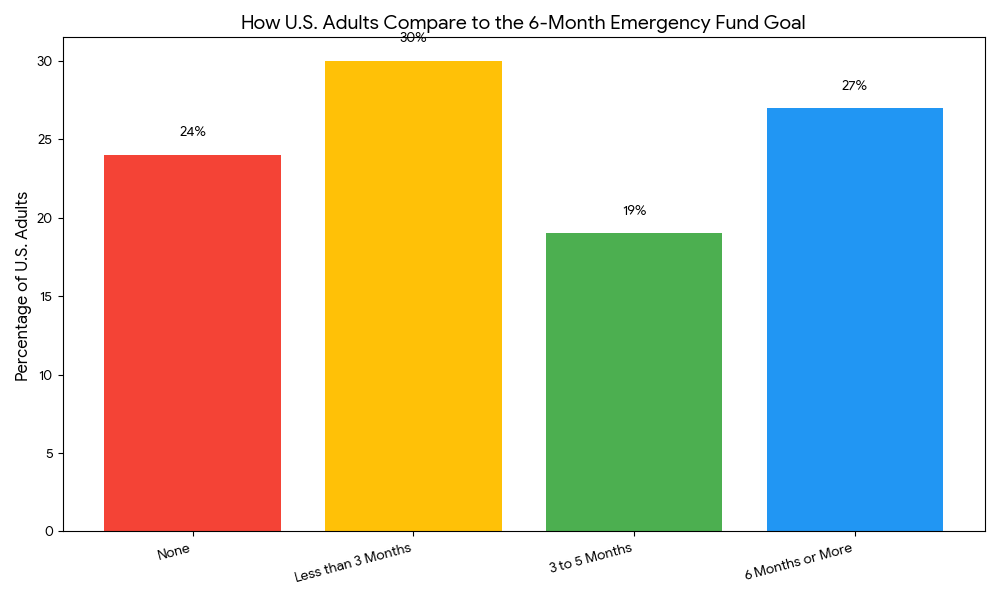

The Current Reality of the 6-Month Goal

Look at the harsh reality of where most households stand compared to the Fully Funded Emergency Fund goal:

This chart shows that even though 3-6 Months Expenses is the recommended norm, only about 27% of Americans actually achieve the six-month level. Your success here is what enables true financial peace and prepares you for the next stages of the Dave Ramsey Baby Steps.

Need help setting up your monthly savings budget to hit these goals? Check out our companion article on how to track your progress: Dave Ramsey Saving Chart Guide

Dave Ramsey Emergency Fund Summary

The goal is freedom. The Dave Ramsey Emergency Fund strategy is your tool to guarantee that life’s messes never put you back into debt.

- Baby Step 1: Get your $1000 Starter Emergency Fund locked down (the fire extinguisher).

- Baby Step 2: Kill all debt (the Debt Snowball).

- Baby Step 3: Build your Fully Funded Emergency Fund (3-6 Months Expenses) to cover any disaster.

Answering Your Burning Questions (FAQ)

What is Dave Ramsey’s emergency fund amount?

It is a two-part answer:

- $1,000 Starter Emergency Fund (Baby Step 1).

- 3-6 Months of Expenses (Baby Step 3).

Is $10,000, $20,000, or $30,000 enough/a good emergency fund?

Yes, likely. Any of these amounts is a good fund if it covers 3-6 months of your essential living expenses. For most households, $20,000 or $30,000 easily covers that six-month goal.

What is the 50/30/20 rule Dave Ramsey?

Dave Ramsey advocates a zero-based budget (giving every dollar a job) but does not promote the 50/30/20 rule. That rule is a general guideline: 50% needs, 30% wants, and 20% savings/debt. Dave’s steps prioritize: Saving $1,000 > Debt Payoff > Saving 3-6 months.

What is the 3-6-9 rule for emergency funds?

The 3-6-9 rule is a general financial planning term suggesting: 3 months for low-risk individuals, 6 months for average-risk, and 9 months for high-risk (self-employed, volatile income, large families). Dave usually only recommends 3-6 months.

What is Dave Ramsey’s 8% rule?

This is a controversial piece of advice regarding retirement withdrawals. The 4% Rule is the traditional guide, but Dave Ramsey suggests that once you are completely debt-free (Baby Step 7), you can sustain an 8% withdrawal rate from an all-stock portfolio. Critics argue this is too aggressive and risky, especially if a market downturn happens early in retirement (Source: Morningstar).

What are the 4 funds Dave Ramsey recommends?

For investing 15% of your income (Baby Step 4), Dave recommends splitting the money equally (25% each) across four types of growth stock mutual funds:

- Growth and Income (Large-cap)

- Growth (Mid-cap)

- Aggressive Growth (Small-cap)

- International

What is the 70-10-10-10 rule for money?

This is a budgeting guideline not related to Dave Ramsey. It splits after-tax income as: 70% Living Expenses, 10% Savings, 10% Investing, and 10% Giving.

Can I retire at 62 with $400,000 in 401k?

It is possible but very tight. $400,000 is considered close to the average retirement savings for that age group. However, retiring at 62 means lower Social Security benefits and a longer reliance on your savings. You would likely need to rely on the traditional 4% withdrawal rule, which only gives you about $16,000 per year before taxes, supplemented by Social Security (Source: SmartAsset).

Learn more about managing your savings and investments by watching this expert discuss your financial journey: Your “Why” Is The Strongest Motivation In Your Financial Journey