How to Nail Your Emergency Fund Monthly Savings Goal (The 01 Easy Way)

Hey there! If you’re here, you’re ready to stop stressing about emergency fund monthly savings goal and start building your financial fortress—that awesome stash of cash called an emergency fund.

Most people get stuck trying to figure out the total number. But let’s be real: you need a monthly savings goal! That’s the secret to actually getting it done.

We’re going to use simple math and smart strategies to figure out exactly how to calculate the emergency fund amount and the monthly action plan to hit it. Let’s make this happen!

Step 1: Figure Out Your “Magic Number” (The Goal)

When calculating your emergency fund amount, you are only counting the things you absolutely must pay to survive for 3-6 months essential expenses if you lost your income.

- Necessities Only: Financial planners like PNC Bank explicitly recommend including things like housing, utilities, transportation, food, and minimum debt payments (Source: PNC Bank).

- The Exclusions: Do not include “wants” like streaming services, hobbies, or extra debt payments. This cash is for survival only.

So, What to Include in Monthly Expenses for an Emergency Fund?

This is where people mess up! An emergency fund is not for splurging. It’s for a true “life happens” moment, like losing your job, an unexpected medical bill, or a car breaking down.

You need to focus on your essential expenses—the things you must pay to survive.

| Essential Expense (Must-Haves) | Non-Essential Expense (Nice-to-Haves) |

| Rent/Mortgage | Eating out/Delivery |

| Groceries (basic food) | Subscriptions (Netflix, Gym) |

| Utilities (Electricity, Water, Basic Phone) | Vacation Savings |

| Minimum Debt Payments (Car loan, Student loan) | Shopping/New Clothes |

| Insurance Premiums (Health, Auto) | Expensive Coffee Runs |

Action Item: Grab your bank statements and a calculator. Tally up only the Essential Expenses from the left column.

Example Calculation: If your total essential monthly expenses are $\mathbf{\$2,450}$, and you choose the 6-month goal (the smart choice!), your total emergency fund target is:

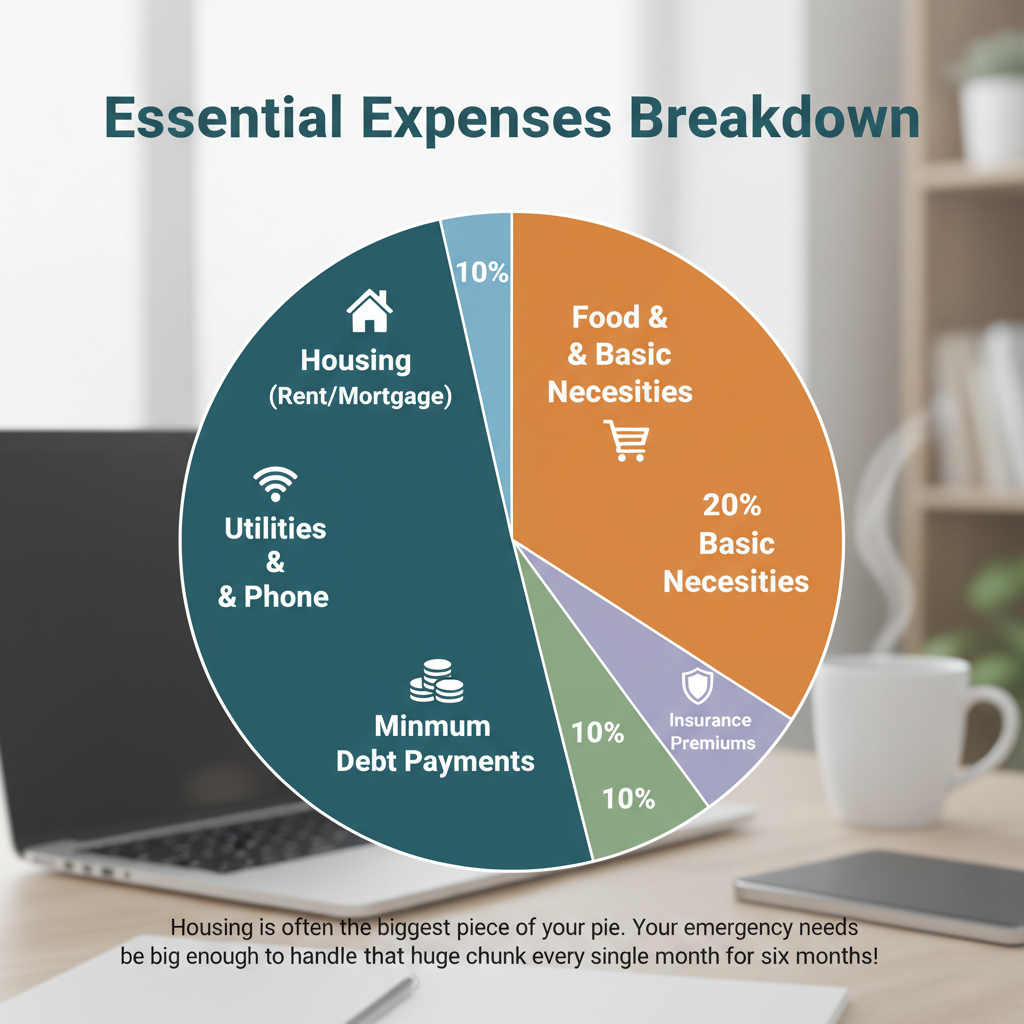

Step 2: The E-Fund Barometer: Are You Covered?

When you look at where money goes, it helps you realize why saving is so important! This visual breaks down a typical household’s essential spending, showing what big parts of your budget your emergency fund needs to protect.

This chart shows that Housing is often the biggest piece of your pie. Your emergency fund needs to be big enough to handle that huge chunk every single month for six months! This kind of analysis helps you see the real-world impact of your savings goal.

Imagine this is a slice of your monthly budget. See how much of it your emergency fund has to cover?

| Essential Expense Category | Percentage of Total |

| Housing (Rent/Mortgage) | 45% |

| Food & Basic Necessities | 20% |

| Utilities & Phone | 15% |

| Minimum Debt Payments | 10% |

| Insurance Premiums | 10% |

Step 3: Setting Your Emergency Fund Monthly Savings Goal

This is where the magic happens. We’ve turned a big, scary number ($14,700) into a simple, manageable monthly goal.

The Formula

Scenario Comparison

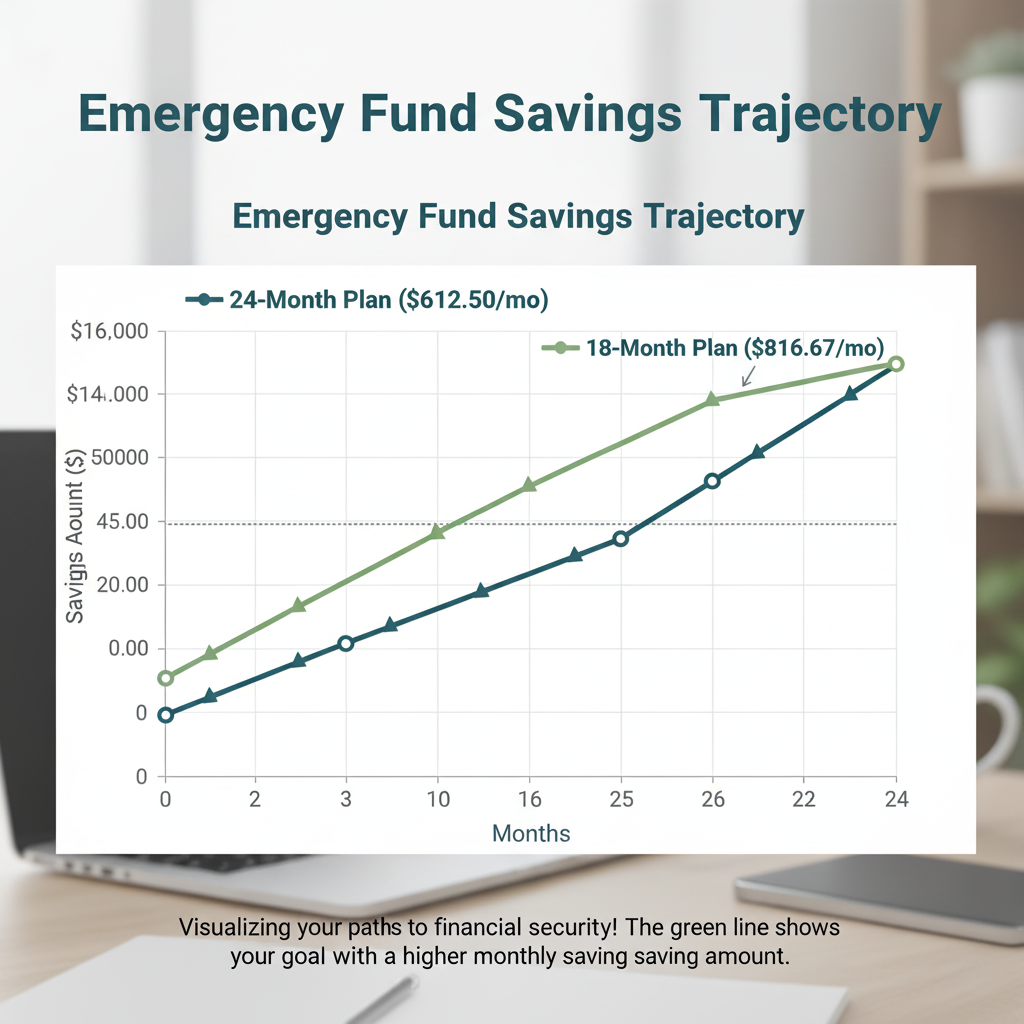

You can set your timeline! Look at how your monthly effort changes based on how fast you want to get there:

| Goal Timeline | Total Goal | Monthly Savings Goal |

| 24 Months (2 Years) | $14,700 | $612.50 |

| 18 Months (1.5 Years) | $14,700 | $816.67 |

This line chart shows how your savings grow over time based on those two monthly goals. See how steady progress adds up!

This looks great! Just one quick adjustment to the line chart description for clarity:

The current description: “Visualizing your paths to financial security! The green line shows your goal with a higher monthly saving saving amount.”

Could be slightly improved to: “Visualizing your paths to financial security! The green line shows reaching your goal faster with a higher monthly saving amount.”

This small change emphasizes the “faster” aspect of the higher saving amount, aligning better with the chart’s visual representation.

Step 4: Where to Keep the Money & Outside Sources

Once you hit that monthly savings goal, where should the money go? The best place keeps it safe, accessible, and earning a little money. For a clearer picture of household financial stability and debt, the Federal Reserve publishes regular reports.

The ideal home is almost always a High-Yield Savings Account (HYSA). You can read more about HYSAs and why safety is key from reliable sources like Bankrate.

Want to know what the average person saves?

We talk a lot about the actual amount people are putting away each month. If you want to dive into the statistics on what people are actually contributing, check out our article: https://itsfinanceguru.com/average-monthly-payment-for-emergency-funds/

People Also Asked (PAA) FAQ Section

We’ve compiled answers to the most common questions people ask when they’re figuring out their emergency fund, helping you master the topic!

How much emergency fund should I have per month?

Your emergency fund monthly savings goal should be the number you calculated in Step 3! It is the Total Goal (3-6 months of essential expenses) divided by your desired Timeline to reach it. For example, if your goal is $14,700 in 24 months, your goal is $612.50 per month.

Is a 3 month emergency fund good?

Yes, a 3-month emergency fund is good—it’s the bare minimum recommended by most financial experts and is a great starting goal! However, a 6-month fund is generally better for added security.

Is 25k a good emergency fund? Is 50k a good emergency fund? Is 10k a good emergency fund? Is 5k a good emergency fund?

The “goodness” of any amount ($5k, $10k, $25k, $50k) depends entirely on your monthly essential expenses. If your essentials are $2,000 per month, $10,000 covers 5 months (which is great). If your essentials are $5,000 per month, $10,000 only covers 2 months (which is not enough). The months covered is what matters, not the dollar amount.

What is the 50/30/20 rule? What is the 70/20/10 rule money?

These are different budgeting guidelines. The 50/30/20 rule suggests 50% to Needs, 30% to Wants, and 20% to Savings and Debt. The 70/20/10 rule is similar but generally suggests 70% to Living Expenses (Needs/Wants), 20% to Savings/Investments, and 10% to Debt. Both rules provide a framework to ensure you are saving enough to hit your emergency fund goal.

How much savings should I have by 40? How much savings should I have by 50?

These relate to retirement savings, not just the emergency fund. A common guideline is to have around three times your annual salary saved by age 40 and six times your annual salary saved by age 50. Regardless of your age, the emergency fund goal remains 3-6 months of essential expenses.

How long will $10,000 last?

$10,000 will last for $10,000 / Your Monthly Essential Expenses months. For example, if your essentials are $2,000, it will last 5 months.

How to save $10,000 in 3 months?

To save $10,000 in 3 months, you must set a monthly savings goal of $10,000 / 3 =~ $3,333 per month. This requires a strict budget and likely cutting many non-essential expenses.

What is a realistic monthly budget?

A realistic monthly budget is one that is based on your actual income and expenses and allows you to consistently hit your monthly savings goal without feeling deprived.

What are the 7 steps in good budgeting?

The seven general steps include: 1) Calculate your income, 2) Track your spending, 3) Set goals, 4) Create a plan (using a rule like 50/30/20), 5) Cut unnecessary spending, 6) Monitor and adjust, and 7) Automate savings.

What are the biggest wastes of money?

The biggest wastes of money are generally recurring expenses that don’t add value, such as unused subscriptions, eating out excessively, and high-interest consumer debt. Cutting these non-essentials is key to hitting your emergency fund monthly savings goal.

How much should a 30 year old have in an emergency fund?

A 30-year-old (like anyone else!) should have 3-6 months of essential expenses saved in an emergency fund. Age is irrelevant; expenses are everything!

Can a person live off $1000 a month?

Whether a person can live off $1,000 a month depends entirely on their cost of living (e.g., rent, location). If their monthly essential expenses are less than $1,000, the answer is yes. If not, the answer is no.

Can you retire at 70 with $400,000?

This is a complex retirement question, not an emergency fund question. $400,000 is likely not enough for a comfortable retirement unless a person has a low cost of living, a substantial pension, or guaranteed income from other sources.

What is the 3-6 9 rule in finance? What is the 2-7-30 rule?

These rules are not standard, widely accepted financial guidelines. Focus on the core recommendation: 3-6 months of essential expenses in a liquid savings account.